Key Takeaways:

- New research1 suggests that the rise in passive investing may have contributed to a self-reinforcing feedback loop that fuels rising stock prices and market concentration.

- In our view, concentrated markets are also a result of unusually strong performance by a small group of companies and changes in the market structure.

- Investors may need to expand beyond public markets to create diversified portfolios.

The Potential Feedback Loop

Passive investing has transformed how investors access the stock market. Rather than trying to outperform an index, passive strategies attempt to replicate the performance of an index such as the S&P 500. Most of these indices are weighted by stocks’ market capitalizations—a company’s stock price multiplied by the number of shares outstanding. This means the largest companies have the greatest influence on returns.

Because passive funds are typically low-cost, they’ve attracted enormous inflows over the last decade. As money flows into these strategies, they automatically buy more of the largest companies in the index.

This contributes to those companies’ share prices rising even more, prompting more buying by active investors who track price momentum (the relative outperformance of a stock or group of stocks). This can create a feedback loop that reinforces momentum and pushes the market toward greater concentration in a handful of large stocks.

The Outperformance of Big Tech

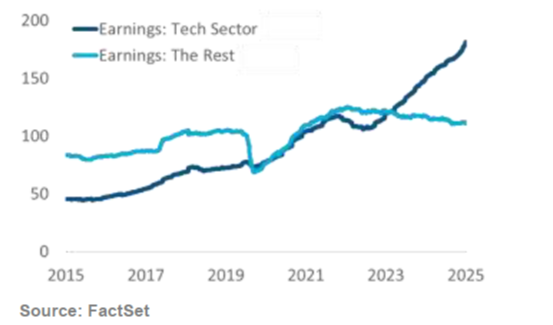

At the same time, large U.S. technology companies have significantly outperformed the broader market. Their superior earnings growth and dominant competitive positions have justified at least some of that performance. For example, in the chart below, we show that earnings growth in the technology sector has far outpaced other sectors over the past five years.

Their strong fundamentals, in combination with strong passive inflows, have contributed to an outsized share of the overall market. Today, a small number of firms—often referred to as the “Magnificent 7”—account for more than one-third of the S&P 500’s total value.

The Changing Market Structure

One lesser discussed contributor to the market concentration trend is a significant shift in the U.S. market structure. In 1995, there were about 8,000 publicly traded companies in the U.S. Today, there are fewer than 4,000. Most of those missing names did not go bankrupt–they went private. As the cost of being a publicly held company increased over the years, many companies were acquired or “taken private” by private investors seeking to manage companies outside of the quarterly pressures of public markets.

Many of these acquisitions were in traditional industries such as industrials, consumer goods, and retail. The resulting public equity market is one that is heavily weighted towards large technology firms. Investors looking to rebalance toward a more diversified representation of the economy and who can tolerate some illiquidity may want to consider adding private markets to their public markets portfolios. Private markets can provide valuable sector diversification—offering exposure to sectors and growth opportunities no longer well represented in public markets.

Summary

The rise of passive investing has done more than lower costs—it has subtly reshaped the character of the markets. By design, market-cap-weighted indexes buy more of the companies that have already gone up, reinforcing momentum and concentrating returns in the largest names. Combined with the strong earnings power of big U.S. technology firms and the shrinking universe of publicly listed companies, that feedback loop has made the market even narrower. Understanding these structural forces is key to building diversified portfolios that reflect the broader economy; this increasingly includes both public and private markets.